| About |

| The Results Wave 28 Wave 27 Wave 26 Wave 25 Wave 24 Wave 23 Wave 22 Wave 21 Waves 11-20 Waves 1-10 |

| Working Paper Series |

| Related Research |

| Authors |

| Sponsors |

| FAQ |

| Contact |

| Press Room |

|

The Results: Wave 6

Paola Sapienza and Luigi Zingales1 April 30, 2010 – Between the passage of sweeping health care reform and an ongoing debate about the projected lifespan of the recession, 23 percent of Americans trust the nation’s financial system, down 2 percent from last quarter’s revised figure, in the midst of dramatic political and economic developments. The latest quarterly findings from the Chicago Booth/Kellogg School Financial Trust Index, issued today, highlight how trust has evolved during the last quarter. The findings also indicate a marked increase in the likelihood of strategic default among homeowners.

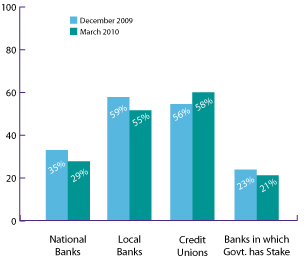

The Chicago Booth/Kellogg School Financial Trust Index is a quarterly look at Americans’ trust in the nation’s financial system, measuring public opinion over three-month periods to track changes in attitude. Co-authors Paola Sapienza (professor of finance at the Kellogg School of Management at Northwestern University) and Luigi Zingales (professor of entrepreneurship and finance at the University of Chicago Booth School of Business), published today’s report as the sixth quarterly update since the inaugural findings were issued more than one year ago. Willingness to Walk Away: Strategic Default on the Rise The researchers found that the number of homeowners willing to default when the value of a mortgage exceeds the value of their house, even if they can afford to pay their mortgage, dramatically increased compared to just a year ago. The percentage of foreclosures that were perceived to be strategic was 31 percent in March 2010, compared to 22 percent in March 2009. One likely reason for this growing trend is the increasing perception that lenders are not going after borrowers who walk away. In December 2009, the average homeowners surveyed said the probability that a lender will go after a borrower is 56 percent, as compared to 54 percent reported in March 2010. “With more and more homeowners believing that lenders are failing to pursue those who default on their mortgages, there is a risk that a growing number of homeowners will walk away from their homes even if they can afford monthly payments.” said Sapienza. The growing importance of strategic defaults is in line with the recent Obama administration’s new set of housing initiatives. The results also indicate that the likelihood of strategic default increases by 23 percent when homeowners learn that their neighbor with negative equity has received a partial loan for forgiveness. Additionally, strategic default increases by 29 percent if homeowners are able to find an alternate way to finance a new home. “A key deterrent to strategic default is the fear of losing a good credit score,” said Zingales. “Approximately 74 percent of homeowners in our survey believe it is very important to maintain good credit and this can be a factor in encouraging them not to walk away.” These findings build upon a paper the researchers released in June 2009 entitled “Moral and Social Restraints to Strategic Default on Mortgages,” which looked at American homeowners’ propensity to strategically default. The paper was the first to analyze and quantify the extent of strategic default during the current recession. Financial Trust Index: Additional Findings In the first quarter of 2010, the Financial Trust Index was at 23 percent, down 2 percent from last quarter’s revised figure. According to the authors, most of this negative change is attributable to banks, which have experienced a steady decline in trust following the stress test process which launched during this time.

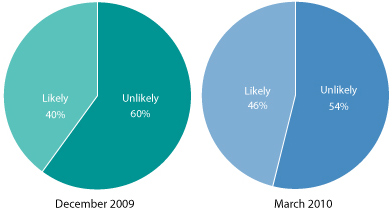

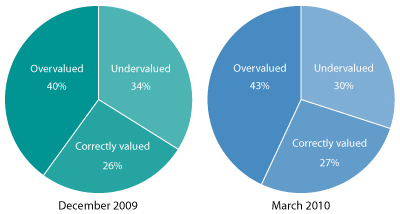

Additionally, fear of a stock market decline showed a marginal increase, as did the fraction of people who think the stock market is overvalued.

The researchers also found that the number of Americans who fear becoming unemployed increased from the revised figure of 21 percent in December 2009 to 26 percent in March 2010. Despite these findings, the expectations on housing prices held steady in the past quarter, with 49 percent of respondents predicting house prices will remain stable and 31 percent forecasting an increase (vs. revised figures of 50 percent and 30 percent, respectively, from last quarter). The authors also found a change in support for government intervention. “Last quarter we reported that consumers were becoming less supportive of government intervention; however, in the first quarter of 2010, we’ve noted a reversal of this trend,” said Zingales. “In fact, our latest data show that more people support caps on executive compensation, government intervention in the way corporations are run and more regulation of the financial sector.”

ABOUT THE SURVEY: On a quarterly basis, the Financial Trust Index captures the amount of trust Americans have in the institutions in which they can invest their money. The survey is conducted by Social Science Research Solutions (SSRS) using ICR's weekly telephone omnibus service. As part of the most recent wave, exactly 1,002 individuals were surveyed March 17 through March 24, 2010. The institutions considered in the survey are banks, the stock market, mutual funds, and large corporations. In the fourth quarter of 2009, SSRS modified its survey sample, approaching respondents via landline and cell phone, versus only landline as had been done in the past. Results from the landline sample only were issued publicly in the January 27, 2010 edition of the Financial Trust Index, though the authors also gathered results for the mixed sample as a point of reference moving forward. The mixed results from the January edition are noted in this press release as revised figures. 1 Paola Sapienza is a Professor of Finance at the Kellogg School of Management at Northwestern University and Luigi Zingales is the Robert McCormack Professor of entrepreneurship and finance at the University of Chicago Booth School of Business. |

|||||||||||||||||||||

{kind=link}